Trust Blog

Explore the latest topics and insights to help you navigate Web3 with confidence and ease.

Follow Trust Wallet on

Introducing the Trust Wallet Agent Kit (TWAK) - Your AI Agent Can Now Act on Crypto

Learn More

Introducing the Trust Wallet Agent Kit (TWAK) - Your AI Agent Can Now Act on Crypto

Trust Wallet Agent Kit lets AI agents execute real crypto transactions across 25+ chains — swaps, DCA, limit orders — within rules you set. Build in under 15 minutes.

What Is Predict.fun?

Learn what Predict.fun is, why its yield-bearing collateral model stands out, and how to access the platform through Trust Wallet today

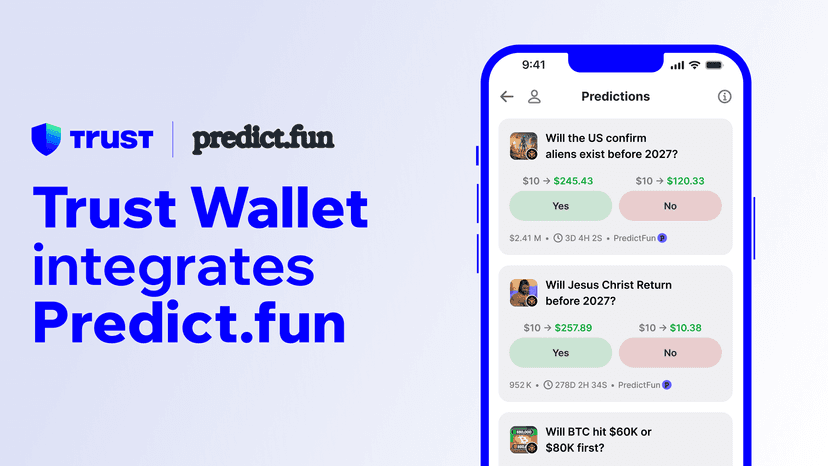

Trust Wallet Integrated Predict.fun Into Predictions

Predict.fun is now live inside Trust Wallet's Predictions tab. Trade sports, politics, crypto, and more on BNB Chain - fully self-custodial, no new apps needed.

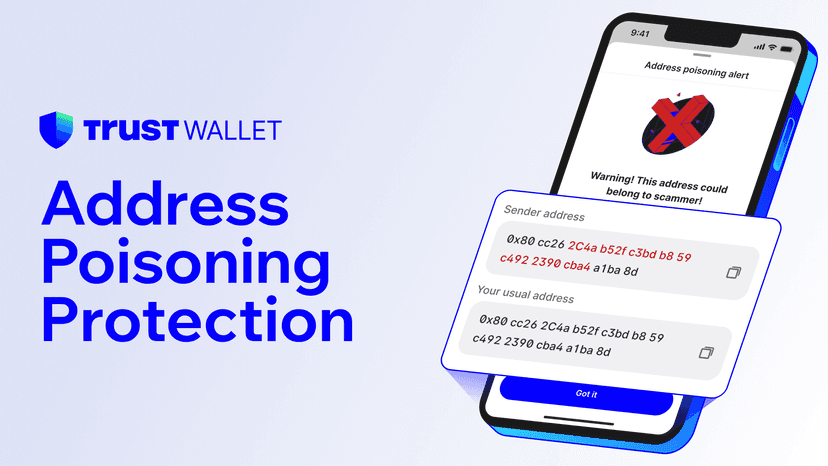

Introducing Address Poisoning Protection on Trust Wallet

Trust Wallet now detects address poisoning in real time. Learn what this scam is, how it targets crypto users, and how we built protection against it.

BRC-20 / Inscription Support Deprecation

Trust Wallet is removing BRC-20 and inscription support. Here's what's changing, why, and what you need to do.

Using Stablecoins for Everyday Money Transfers: What to Know

Learn how stablecoins make everyday money transfers faster and more affordable, and how Trust Wallet helps you store, send, and earn with them.

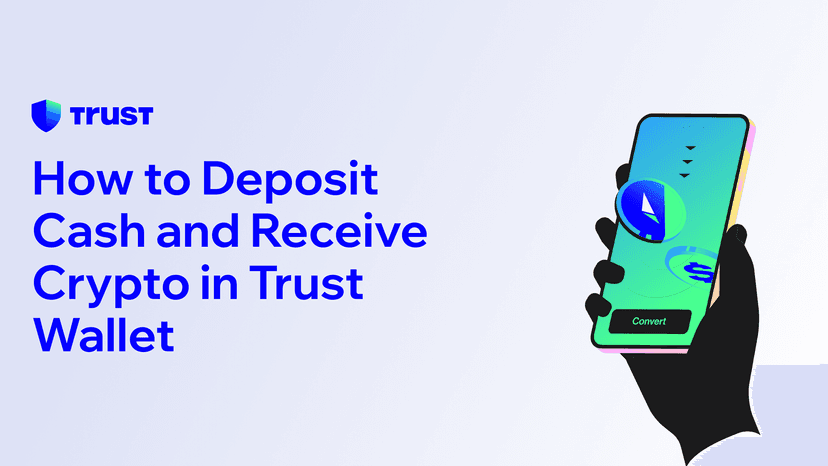

How to Deposit Cash and Receive Crypto in Trust Wallet

Learn how to deposit cash and receive crypto directly in Trust Wallet using Coinme's cash-to-crypto service at retail stores across 48 U.S. states*.

How to Fund a Crypto Wallet With Cash (No Bank Account Needed)

Learn how to fund your crypto wallet with cash – no bank account needed. Use Trust Wallet's Cash Deposits feature powered by Coinme at 48+ US states & Puerto Rico

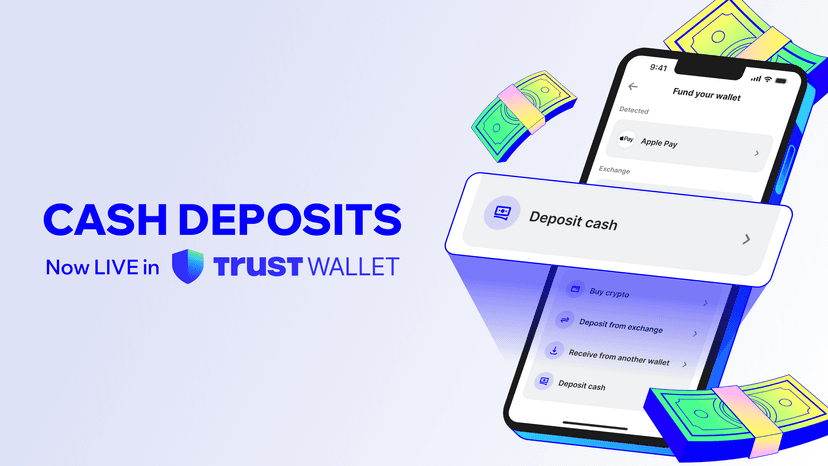

Introducing Cash Deposits on Trust Wallet: Turn Cash Into Digital Money

Turn physical cash into digital money with Trust Wallet. Deposit cash at nearby U.S. retail locations and receive crypto after network confirmation, no bank account required.

How to Use QR Payments in Vietnam with Trust Wallet

Learn how Trust Wallet lets you initiate QR payment flows in Vietnam using VietQR codes. Users spend digital assets from their wallet while merchants receive local currency through a settlement partner.

What is Polymarket?

Discover Polymarket, the world's largest decentralized prediction market. Trade on real-world events using USDC on Polygon blockchain with transparency.

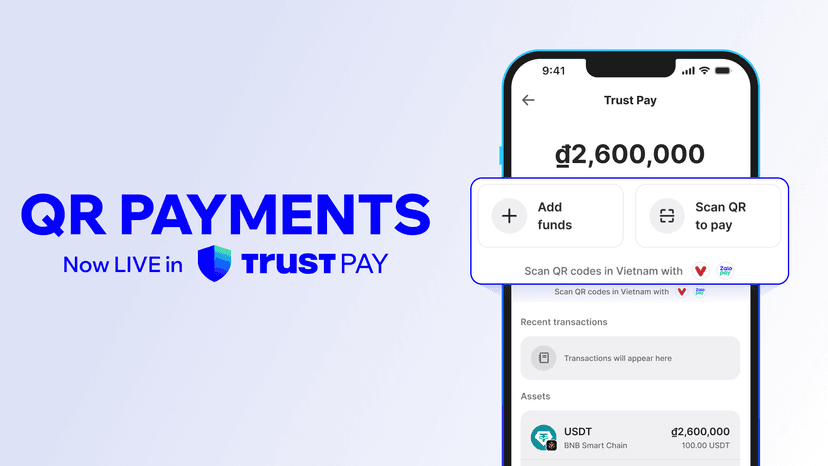

Introducing QR Payments: Spend Stablecoins in the Real World

Use stablecoins to initiate QR payments via Trust Wallet. Merchants receive local currency instantly, while you stay fully self-custodial.