Блог Trust

Изучите последние темы и информацию, которые помогут вам уверенно и легко ориентироваться в Web3.

Подписаться на Trust Wallet вИзучите последние темы и информацию, которые помогут вам уверенно и легко ориентироваться в Web3.

Подписаться на Trust Wallet в

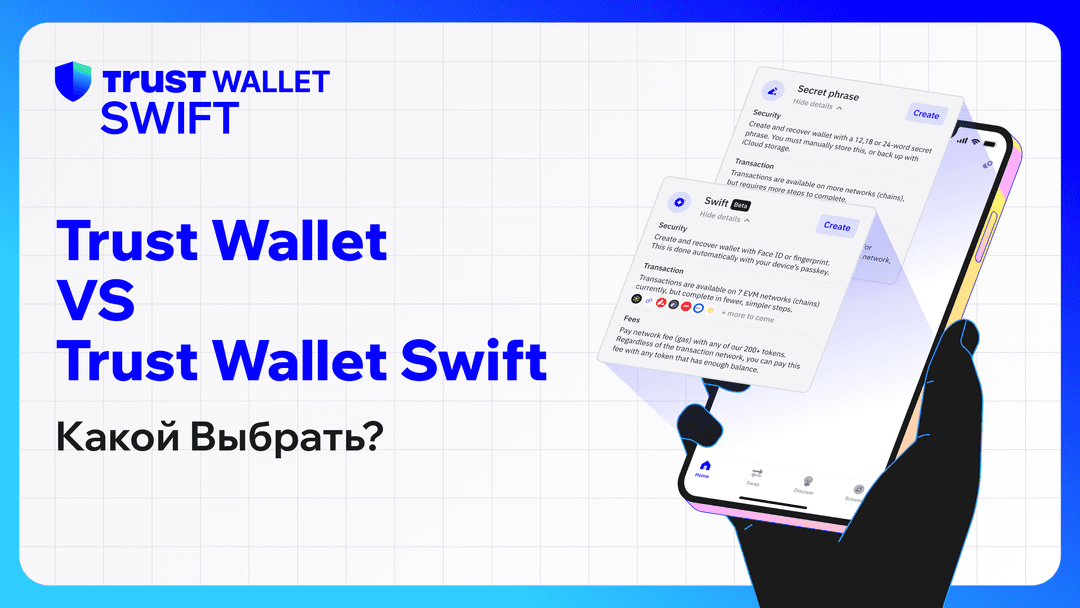

Узнайте о ключевых различиях между Trust Wallet и Trust Wallet SWIFT в этом руководстве. Узнайте, как выбрать лучший кошелек Web3 для ваших задач.

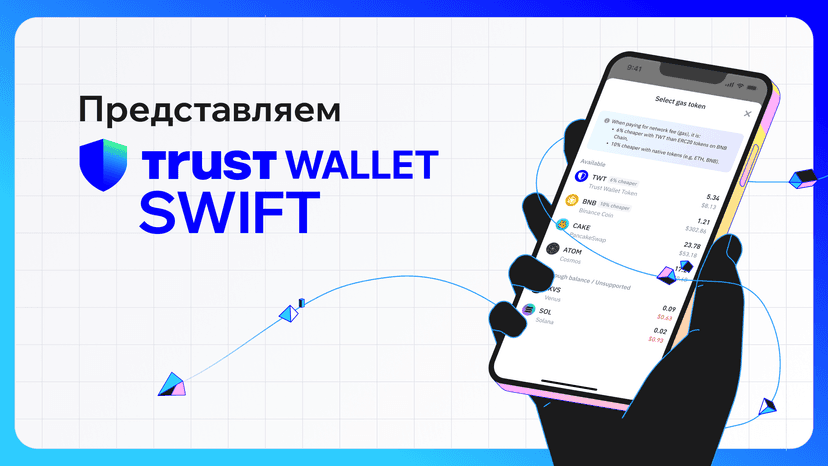

В этой статье мы расскажем, как оплатить газ с помощью TWT для перевода токенов с помощью Trust Wallet Swift.

Откройте для себя Trust Wallet SWIFT: самый простой способ начать знакомство с Web3. Узнайте, как благодаря абстракции аккаунтов, он предоставляет бесшовный и безопасный опыт взаимодействия с Web3.

Trust Wallet получил сертификаты ISO 27001 и ISO 27701. Это достижение является свидетельством нашей приверженности поддержанию самых высоких стандартов безопасности и конфиденциальности в сфере криптокошельков.

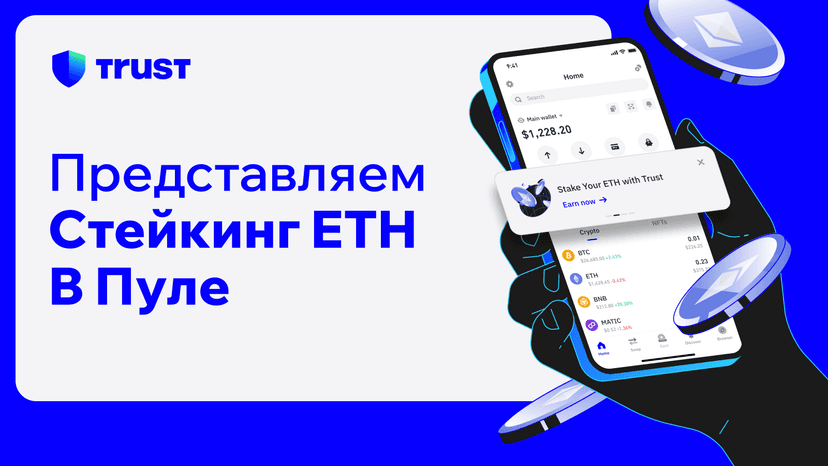

Начните зарабатывать криптовалюту с помощью стейкинг-пула ETH в Trust Wallet, функционирующего на базе Kiln. 32 ETH более не требуются. Начните всего с 0,025 ETH.

Играйте в AI Hero, используя Trust Wallet, и выигрывайте долю из $2500! Эксклюзивное предложение для нашего CНГ сообщества! Первые 400 новых игроков, которые начнут играть с использованием Trust Wallet, получат вознаграждение в размере $5 в $BNX.

Исследуйте криптоигры: руководство для новичков по играм с возможностью заработка, NFT и заработку реальных наград. Подключитесь к Trust Wallet для новой эры в мире игр.

Исследуйте революционные изменения Web3 с нашим руководством: от понимания децентрализованных кошельков Web3, таких как Trust Wallet, до безопасного перемещения по децентрализованной сети.

Исследуйте ключевые факторы, влияющие на цену биткоина, включая динамику предложения, изменения в регулировании, технологические достижения и психологию рынка в нашем руководстве.

Узнайте об изменениях в поддержке сети Trust Wallet для Aion (AION), Nebulas (NAS) и Viacoin (VIA). А также получите инструкции по миграции ваших активов, если у вас есть активы на этих конкретных блокчейнах. Обновление поддержки сети Trust Wallet: Aion, Nebulas и Viacoin

Миссия Trust Wallet всегда была сделать мир Web3 интуитивным, безопасным и открытым для всех. Мы с восторгом объявляем о нашей интеграции Mantle Mainnet, предоставляя вам еще больше возможностей и обогащая ваш опыт в мире децентрализованных приложений (dApps) и управления цифровыми активами. Этот гид создан для того, чтобы помочь вам ориентироваться и извлечь максимум из этой новой интеграции в Trust Wallet.

Откройте для себя преобразования в экосистеме Polygon с введением токена POL вместо MATIC. Также узнайте, как использовать Trust Wallet для взаимодействия с этой развивающейся сетью.